National Energy Services Reunited (NESR)·Q4 2025 Earnings Summary

NESR Delivers Record Revenue as Jafurah Ramps to $2B Run Rate Exit

February 17, 2026 · by Fintool AI Agent

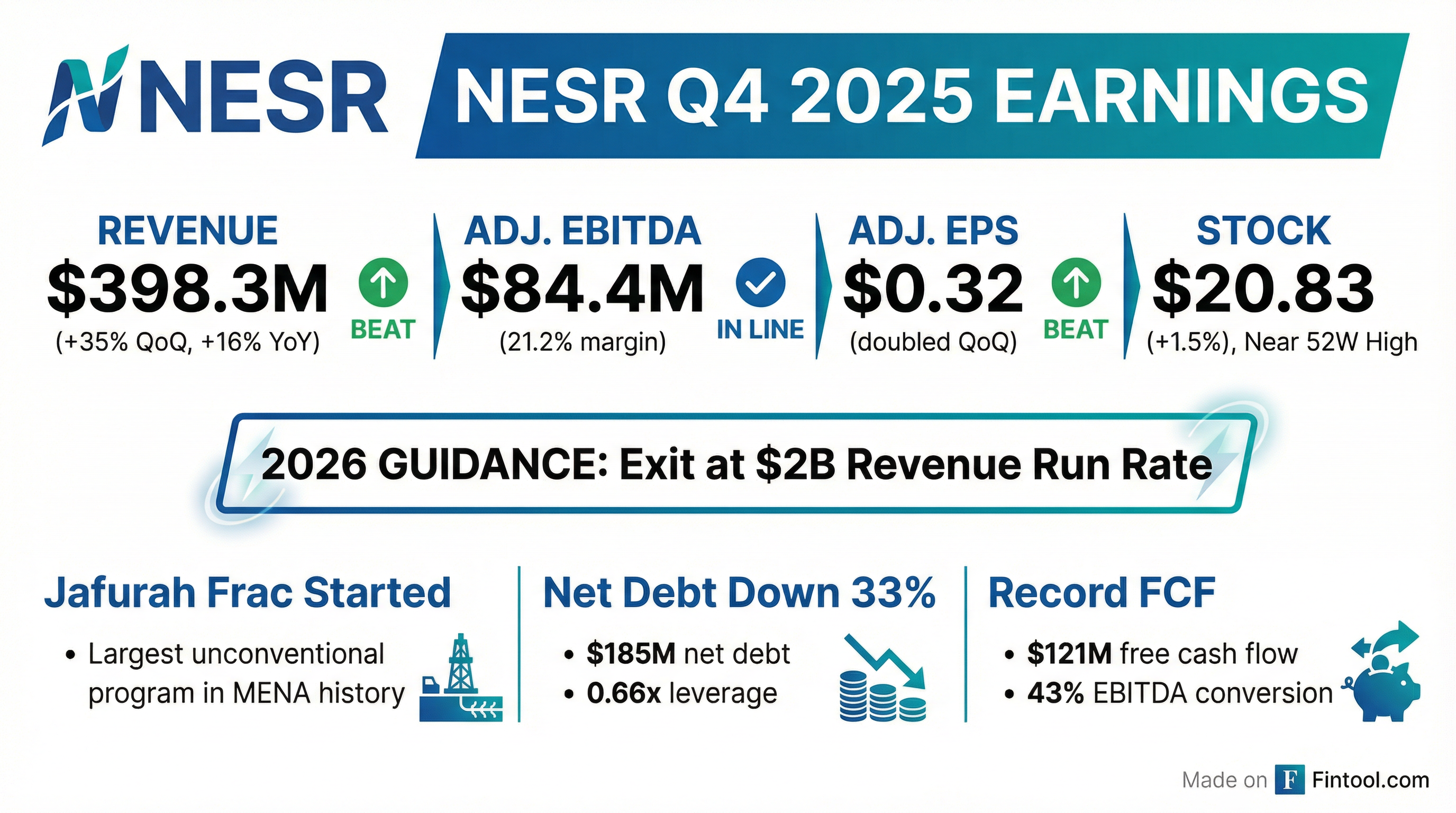

National Energy Services Reunited Corp. (NESR) posted record quarterly revenue of $398.3 million in Q4 2025, surging 34.9% sequentially and 15.9% year-over-year as the MENA-focused oilfield services provider began mobilizing on Aramco's Jafurah unconventional development. Adjusted EPS more than doubled to $0.32, while management guided to exiting 2026 at an annualized $2 billion revenue run rate.

CEO Sherif Foda framed the quarter as a major milestone: "The fourth quarter represents a significant milestone for the company, not just in terms of hitting ambitious growth targets, but also in proving that we can do so profitably and with strong cash flow generation."

Did NESR Beat Earnings?

Revenue exceeded expectations with a step-change in activity levels driven by Jafurah contract mobilization:

CFO Stefan Angeli highlighted: "Margins remained stable due to strong cost discipline, improved operational execution across our portfolio, and the continued benefit of our lean overhead structure."

What Did Management Guide for 2026?

Management provided explicit quantitative guidance for the first time, reflecting high visibility from the contract backlog:

CFO Stefan Angeli noted: "Overall, this year should be our best growth year ever, exceeding any previous indication."

How Did the Stock React?

NESR shares have been on a remarkable run, gaining 300%+ from the 52-week low of $5.20:

Values retrieved from S&P Global

The stock is trading near all-time highs, reflecting confidence in the Jafurah contract and broader MENA expansion.

What's the Latest on Jafurah?

The Jafurah unconventional frack program with Aramco is the largest in MENA history and represents a transformational contract for NESR. Key operational details from the call:

CEO Sherif Foda emphasized the supply chain advantages: "All of this was basically solved, and that's why I keep saying it's just we are at Aramco, our client, whenever they ask for additional stuff, we just require a couple of weeks to be ready."

On margin optimization potential: "We believe that we can do more stages per day... If we do that, that means that you can get another 20% efficiency, which will definitely have an impact on our margins."

What Changed From Last Quarter?

Q4 2025 marks a clear inflection point with several catalysts converging:

-

Jafurah Revenue Contribution — First full quarter of mobilization revenue, with ramp continuing through 2026

-

Revenue Stepped Up 35% — From $295M to $398M in a single quarter, signaling the "totally different gear and scale"

-

$2-3B Tender Pipeline — Majority of tenders submitted and awaiting awards throughout 2026

-

Path to Double the Company — CEO outlined plan to double NESR by 2027 through contract wins

-

Shareholder Returns Coming — Will announce formal capital allocation framework next quarter

Country-by-Country Growth Outlook

Management provided detailed commentary on each key market:

Kuwait — Becoming #2 Market

- Spending Commitment: $8-10 billion per year upstream through 2030

- Capacity Target: 4 million barrels per day by 2035 (up 1M bbl/d)

- IOC Entry: Total, BP, Shell, and others signed MoUs at KOGHS

- NESR Position: "We can easily double the size of our business in Kuwait"

- Tenders: All awards expected in 2026 (Q1, Q2, Q3), contracts for 5-7 years

- Innovation: First-ever access to technology development via Ahmadi Innovation Valley (AIV)

Abu Dhabi — All-Time High Activity

- Investment Plan: ADNOC approved $150 billion for 2026-2030

- Activity: "Continues to march at or above all-time high"

- Outlook: "Should keep the growth trajectory intact for years to come"

Libya — Unprecedented IOC Commitment

- Major Deals: ConocoPhillips + Total: $20 billion over 25 years

- New Exploration: Chevron, Repsol, MOL awarded new blocks

- Capacity Target: 2 million bbl/d by 2030 (from 1.4M today)

- NESR Position: "For us to triple the company or the size of NESR in Libya is not a big deal"

Saudi Arabia (Ex-Jafurah)

- Rig Additions: 40-60 rigs expected in 2026

- LSTK Tenders: "Huge tender backlog" for lump sum turnkey contracts

- Market Share: NESR expects to maintain share on incremental rigs

Syria — Monitoring Entry

- Status: Sanctions lifted, in discussions with leadership

- NESR Advantage: 75 Syrian employees already in the company

- Opportunity: Revitalization of Deir ez-Zor (historically 500-600k bbl/d)

Capital Allocation Update

CFO Stefan Angeli outlined the balance sheet strength and upcoming shareholder return framework:

Shareholder Returns: "We expect to provide an update on our formal capital allocation and shareholder return framework during our next earnings call... Everything's on the table. Dividends, stock buybacks, etc."

Full Year 2025 Performance

Full-year revenue was relatively flat as NESR invested in capacity ahead of major contract awards. The Q4 step-up and explicit $2B run rate guidance suggest 2026 should see 50%+ revenue growth.

Q&A Highlights

On Jafurah Ramp Timeline (David Anderson, Barclays)

Q: Where are we today in terms of the ramp-up at Jafurah?

A (CEO Foda): "By Q2, I think we would be in that kind of steady state, and then we might add another fleet in Q3, Q4. And the run rate for our stages per quarter should be seen very clearly in Q3."

On Margin Optimization (Suraj Pant, BofA)

Q: Where are those incremental efficiencies going to come from?

A (CEO Foda): "We believe that we can do more stages per day... you can get another 20% efficiency, which will definitely have an impact on our margins."

On CapEx Requirements (Josh Silverstein, UBS)

Q: What level of investments might you need to support these higher activity levels?

A (CEO Foda): "We have a $150 million-$180 million CapEx timeframe. If we win much more than what we even think we're gonna win, we might get this to $200 million."

On Doubling the Company (David Anderson, Barclays)

Q: What feeds into the greater than $2 billion number?

A (CEO Foda): "We tender $2-$3 billion of tenders across the region. Most of it is submitted. The majority of it is outside Saudi. When you win these contracts and you start them, then you would be able to exit with a much higher run rate than previously anticipated."

Historical Beat/Miss Record

NESR has delivered consistent earnings beats in recent quarters:

Values retrieved from S&P Global

Key Risks and Watch Items

-

Jafurah Execution Risk — The contract is transformational but requires flawless mobilization at unprecedented scale

-

Tender Award Uncertainty — $2-3B pipeline depends on winning "more than fair share" of competitive tenders

-

Geographic Concentration — MENA focus creates exposure to regional geopolitical risks

-

Customer Concentration — Aramco relationship is critical; any change in spending priorities would impact NESR significantly

-

Margin Trajectory — Adj. EBITDA margin contracted 420 bps YoY; watching for stabilization as Jafurah scales

What To Watch Next

Q1 2026 Earnings (Expected May 2026):

- Jafurah revenue ramp and stages per quarter

- Margin recovery as mobilization costs normalize

- Kuwait and other MENA tender award announcements

- Shareholder return framework announcement

Near-Term Catalysts:

- Tender awards across Kuwait, UAE, and North Africa (Q1-Q3 2026)

- SPARK facility completion (Q3 2026)

- Potential entry into Syria

Conference Call Details

The conference call was held 8:00 AM ET on February 17, 2026.

- Webcast replay available at investors.nesr.com

- Full transcript available

This analysis is based on NESR's Q4 2025 earnings call transcript and 8-K filing published February 17, 2026. Adjusted metrics are non-GAAP measures; see company filings for reconciliations.